Overview

This is one module within a broader toolkit intended to facilitate the goals and projects of First Nations communities related to housing and homelands governance. Each module can be used individually, in connection with other supporting modules, or in conjunction with the toolkit as a whole-system approach.

One of the enduring challenges for First Nations housing is the lack of opportunities for financing and lending for new construction, particularly for First Nations governments and individuals seeking to build on their lands. Various mechanisms have been created over the years to overcome some of these obstacles, but challenges remain.

This module has been created to offer insight into the factors that can make or break a financial relationship, from the perspective of financial institutions and lenders. It also outlines innovative ways to source financing outside traditional methods.

Download First Nations Housing Financing: Sources and Factors Module

Key Factors that Financial Institutions and Lenders are looking for

Below, we list factors that affect lending for two types of relationships: a) between a financial institution and a First Nation Government, and b) between a financial institution and an individual member of a First Nation community.

Factors that affect the lending relationship of a financial institute with a First Nation Government:

Relationship: Our findings indicate that one of the key factors, if not the most important one, is a trusted relationship and track record of lending success between a financial institute and a First Nation government. Building an early relationship with a financial institute and including them in discussions regarding the development of new housing and land governance regimes can facilitate a positive long-term lending relationship.

Tenure Security: In lieu of fee-simple private ownership regimes, financial institutes will still require secure, transparent, long-term tenure regimes. For many First Nations on-reserve or on treaty lands, this means registering long-term leases under relevant legislation. An alternative for First Nations beyond reserve and treaty lands could be to structure long-term leases under Community Land Trusts, which may be an optimal structure to facilitate financial lending.

Ability to Backstop: Financial institutions prefer lending to First Nations who can guarantee a loan. This can be done by way of band council resolutions, registered land codes, loan agreements in which the First Nation government is a party, and the creation of specific housing buy-back funds for members. In the absence of backstopping abilities, another option is negotiating loans to build non-permanent (i.e., easily moved) structures that are independent of the land title and that could be physically collected as an asset by a bank in the case of default.

Good Data: Financial institutes will look favourably upon governments who have detailed data on the state of housing and needs, including the number and kinds of houses, such as rental or multi-generational, their condition, repair requirements, overcrowding, and other factors including Level of Service requirements.

Strong Codes and Policies: Instituting a housing policy and land code that contains clear and transparent rules and processes related to housing and land allocation, use, enforcement, and redistribution is critical for First Nations seeking financing. The formulation of culturally legitimate codes and policies can be an important opportunity to integrate the values and principles of a community with the institutional requirements found in this module.

Income, Economies, and Assets: The ability to demonstrate consistent economic activity and the availability of diverse income sources demonstrates that: a) a First Nation government can guarantee loans; and b) economic opportunities exist for individual housing residents. Economic activity can include a mix of income sources such as grants, loans, internal taxes, business revenues, and royalties. It could also potentially include economic assets held by the First Nation, including natural resources.

Housing Market: Housing construction occurring within a geographic area deemed to be desirable can increase potential for lending. For many rural First Nations communities, housing markets can potentially emerge on their lands through the combination of security of tenure via leases or other agreements, a desire among members to return to their homelands, and increased commercial and/or tourism opportunities within their territory.

Appropriate Infrastructure: Financial institutes prefer to see the availability of supporting physical and social infrastructure for housing. This includes connecting roads, lots that are appropriately developed and zoned with service availability, and adequate utility provision. It can also include innovative housing support systems for residents (see for example the CLT Module).

Factors that affect the lending relationship of a financial institute with an individual member of a First Nation:[1]

Credit: For any individual, a good credit score is key to accessing financing for housing. The minimum score required is usually around 680 to 690 on their scale. Credit ratings can improve over 12 months and there are numerous ways for individuals to improve their credit rating.

Financial Literacy: Being able to demonstrate financial literacy as an individual can be an important factor in receiving a loan. Financial literacy programs are usually free and may be offered by a First Nation government, or at credit unions or banks. It is advisable to keep certificates of completion or other records of completing such programs.

Down Payment: The ability to make an adequate down-payment is an important factor in the willingness of a financial institute to lend to an individual. This can be demonstrated through personal savings accounts, RRSPs, inheritances, settlement funds, compensations, and support provided by a First Nation government or other entity such as a Community Land Trust via a Shared-Equity arrangement.

Factors that can help build credit scores:

Opening a bank account. This provides evidence of a financial history and allows individuals to make electronic transactions and provide the documentary proof required during mortgage applications.

Payment of rent and utility bills using digital options for record-keeping where possible. Where not possible, save copies of physical receipts. A responsible payment history builds trust that a debtor will honour mortgage obligations without defaulting.

Using and repaying prepaid cards or credit cards to build or improve credit score, which shows responsible use of funds. Transaction history can demonstrate to a potential loan provider that the candidate has desirable spending patterns such as budgeting for necessities and leaving margins for savings.

Paying off smaller debts like vehicle loans and personal loans, paying off credit card debt, and paying expenses in installments on credit cards. Lower liabilities can inspire confidence that debtors will make mortgage payments on time.

[1] All financial institutes with whom we spoke indicated that the Federal Government of Canada does not allow any form of leniency in terms of the listed lending norms and criteria for First Nations individuals.

Alternative Funding Sources and Regimes

The following are a few examples of strategies that can be used to both source and structure financing for housing or other purposes in innovative ways that don’t rely solely on bank loans or government funding.

Housing Loan Funds

A Housing Loan Fund (HLF) is a local, grassroots financial instrument established by a First Nation or group of First Nation communities. An HLF can be designed with varying levels of sophistication, but always with a primary purpose of extending housing construction and renovation loans to members of associated First Nations.

The advantage of establishing a Housing Loan Fund is that a First Nation can create its own risk management strategy, relying on their own chosen metrics rather than credit scores, and accepting forms of collateral that may not be considered by conventional financial institutions.

First Nations can explore innovative ways to capitalize housing loan funds, including:

- Securing significant loans from a bank, asset management company, private equity company, or social impact investor

- Allocating settlement funds or transfer payments from the Federal government

- Redirecting profits from community-owned businesses toward a housing fund

- Pooling resources from members

Customized HLFs can also be combined with shared-equity financing and ownership options, which may increase access to a larger number of individuals.

Social Impact Bonds

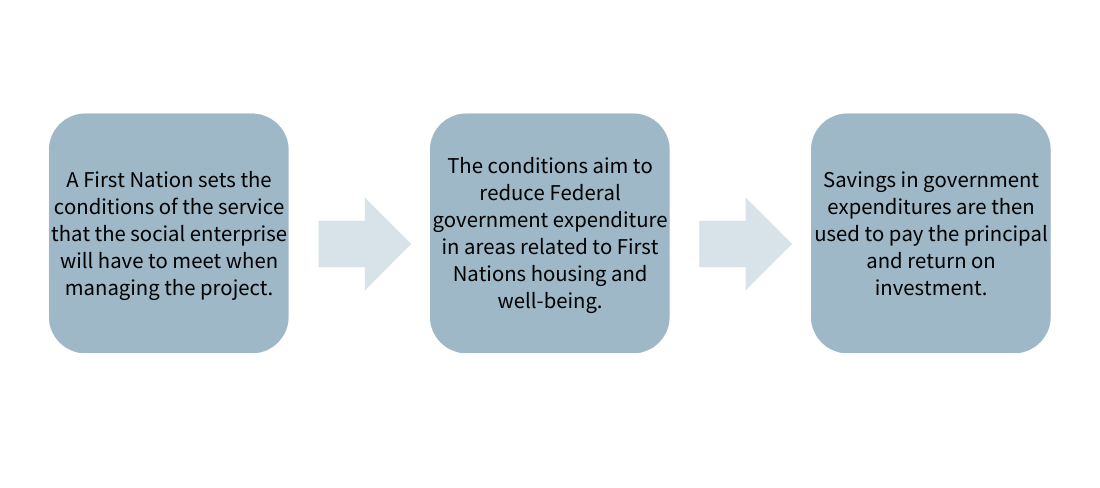

The Canadian federal government spends millions of dollars on First Nations housing annually, even though many of those expenditures are failing to result in concrete improvements in the lives of First Nations people. SIBs are built upon the premise that the social impacts resulting from certain projects and activities carried out within the not-for-profit and social enterprise sector can equal cost savings in terms of government expenditures.

Social Impact Bonds (SIBs) have not yet been extensively explored within the context of First Nations housing but may offer an alternative pathway toward financing much-needed housing projects and related activities. SIBs are a financial instrument meant to aid financing gaps for socially responsible projects. They can be used to build new homes, repair existing homes, build rental homes that can be given at subsidized rates, or a combination of these options.

SIBs allow First Nations to set the parameters and conditions of the housing-related services and projects that are needed, rather than having to design projects around constrained government funding. When SIBs are successful, the government then repays the social impact investor at a designated rate of return.

SIBs typically rely on the cooperation of numerous parties in order to function: the financial institutes who issue the bonds, the social enterprise entities who manage the housing development/activity, the government who pays out the bonds, and the social impact investors themselves.

Labour Value Contributions (aka Sweat Equity)

Sweat equity, understood as labour contributions from individual owners during the construction phase of a home, perhaps receives the least amount of attention as a form of First Nations housing funding. Technically, it should be considered an alternative subsidy for housing, in that it can be combined with conventional housing funding and financing or with the opportunities listed above.

Sweat equity is valuable in that, in addition to cost-savings, it can potentially provide significant social returns to the community in terms of:

- Sense of ownership and pride in homes

- Capacity-building and skills training

- Meaningful employment

- Community cohesion and participation

- Lower construction costs

Targeted sweat-equity subsidization programs can be developed to ensure that local participation in building projects include:

- Formal training and certification

- Participation early on, from the design stage onward

- Follow-up support for participants

- Enterprise development

A sweat-equity relationship between neighbouring communities could also be particularly productive if their interests and capacities intersect.

For example, suppose Nation A and Nation B both want to build houses in their communities. Nation A has access to lumber on their traditional territories, perhaps even a small sawmill, but lacks skilled labour such as lumberjacks and carpenters. Nation B lacks the primary lumber resources but has supported the training of several members of their community to become certified and skilled in turning raw lumber into usable wood products. Neither Nation A nor Nation B can afford to pay the other Nation for what they need from their current monetary budget. It would clearly be beneficial to both parties to develop a local agreement of exchange to enable the work.

Sweat Equity can help communities, both internally and between neighbours, to overcome hurdles to housing development where collectively there is sufficient raw resources and potential skilled labour, but there are challenges related to insufficient funding and/or cooperation.

Next Steps

- Approach relevant financial and/or government institutions and enquire whether they would be interested in partnering to facilitate one or more of the above solutions.

- Continue reading other modules in the toolkit to deepen understanding in connected areas such as Community Land Trusts for a potentially helpful approach to collective housing management and Shared Equity for more accessible individual housing finance.

- Reach out to the Indigenous Home-Lands initiative at Ecotrust Canada. We’re ready to offer support to First Nations partners interested in delving further into any of the concepts presented here. To learn more, contact us via https://ecotrust.ca/priorities/home-lands/